The state of Hormuz: oil price action is not the story

May 5, 2026 at 6:12 AM

Another month, another week, another batch of headlines, and new all-time highs for US stock markets might not be the news one awaits when they see the recent flip-flopping in oil prices. The first thing worth saying about the past forty-eight hours around the Strait (not state: pun intended) is what did not happen.

WTI did not break $110. Brent gave back roughly $5 between Monday's peak and Tuesday's trough (for now). Meaningful gains stand since the open on the 4th of May, but we’re nowhere near panic levels. From the open on Monday morning to the current quotes on Tuesday afternoon in London, WTI moved from $101.50 to over $109, and Brent, from $110 to above $120. The four-year high on Brent was a potential double top formation in tandem with the30th of April. This most recent spike was marked by an Iranian claim of striking a US frigate that the US subsequently denied and the news was refuted later by the Iranian Fars news agency.

If you read those tape moves and conclude that the oil market has digested Iran's strike on the UAE, the limited results of Trump’s "Project Freedom" announced over the weekend, and the UAE's near-simultaneous departure from OPEC+ (effective May 1) and OAPEC (announced May 3), you are reading the screen and not the situation.

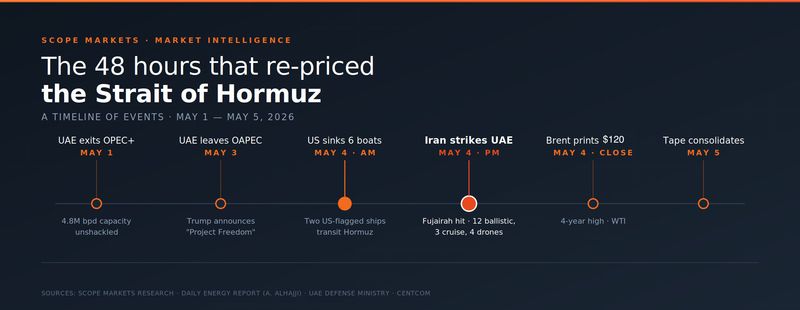

What actually happened, in order

May 1. Last week’s announcement of UAE's withdrawal from OPEC and OPEC+ took formal effect. The third-largest OPEC producer is gone, with 4.8 million barrels per day of capacity and no quota constraint. That said, the country can barely export around 1.7 mln barrels per day through the port of Fujairah on the other side of the Strait of Hormuz.

May 3. The UAE also withdrew from the Organization of Arab Petroleum Exporting Countries (OAPEC). Most oil-market journalists missed it entirely, despite OAPEC's substantial role in regional shipping, training, and joint investment vehicles like the Arab Energy Fund. Oil markets analyst, Dr. Anas Alhajji, flagged it the next day in his Daily Energy Report and used the moment to point out that very few people writing about Gulf oil actually understand what OAPEC is.

May 3 (evening). President Trump announced "Project Freedom" - use of the US Navy to escort commercial vessels out of the strait of Hormuz.

May 4 (morning). US helicopters sank six or seven Iranian small boats. Two US-flagged vessels transitted successfully through the strait. WTI opened at $99.73 and printed a high of $107.46.

May 4 (afternoon). Iran launched a coordinated attack on the UAE. The UAE Defense Ministry confirmed its air defenses engaged 12 ballistic missiles, three cruise missiles, and four drones. A drone ignited a fire at the Fujairah oil terminal - the same Gulf-of-Oman pipeline hub the UAE built specifically to bypass Hormuz. Brent closed near $114.44, which is still very much near four-year highs.

May 5 (today). WTI faded to $103.92, while a ship belonging to Maersk transitted through the strait. Nevertheless over 2,000 vessels remained stranded in the Gulf.

Timeline of events around the Strait of Hormuz crisis - May 2026

Price action not bullish enough

A four-percent Brent rally on a day when Iran hits a Gulf petroleum hub for the first time since the April 8 ceasefire, all the while the world's third-largest OPEC producer has just unshackled its spare capacity but cannot ship it, is not the price action of a market that has properly absorbed what just happened. It is the price action of a market that is still trading the headline and not the structure.

Alhajji captured the asymmetry well in his May 4th note. His warning to readers, almost in passing, was that "markets can crash abruptly once business leaders acknowledge the recession is already underway."

Sit with that for a moment. If we are already in a recession that has not yet been recognized, then the relevant question for crude is not "how high can it go." It is "what happens to crude when an unrecognized recession suddenly becomes a recognized one, against the backdrop of structural Gulf supply loss." Those two forces pull in opposite directions on flat price, and the curve right now does not appear to be paying for a swift move in either direction.

Fujairah is the only word that matters

The narrative coming out of Washington is that Project Freedom is making progress because two US-flagged ships made it through. The narrative coming out of Tehran is that the strait remains effectively closed. Both are true, but neither of the two is the story - that is rather that Iran chose Fujairah.

The UAE's exit from OPEC+ is only economically meaningful if Abu Dhabi can actually export the additional barrels it intends to produce. Hormuz is closed. The Fujairah terminal which is only capable of moving roughly 1.7 million bpd in 2025 was the bypass. By striking Fujairah on May 4th, Iran sent a message that goes well beyond the war: your post-OPEC strategy depends on infrastructure we can reach. A single drone fire that injures three workers does not, by itself, take Fujairah offline. But it changes the insurance math, the operational risk premium, and the long-horizon investment case for every carrier and refiner that was about to commit to Gulf-of-Oman lifting as the new normal.

This is also why the Saudi response matters more than it appears. Riyadh condemned the strikes on the UAE, but Riyadh is not naturally aligned with an Abu Dhabi that has just walked out of the oil cartel and is preparing to compete on volume. The two countries' rivalry over Yemen, the Red Sea, and now production policy is the silent variable underneath everything that happens next.

The concept the market is not pricing: demand destruction

The need for traders to be able to distinguish between temporary demand decline and demand destruction is now urgent. Temporary declines rebound when prices ease. Demand destruction is permanent as airlines start to retire fleets. Manufacturers re-shore, while trucking margins compress until small operators leave the industry. Consumers learn to drive less and do not unlearn it. Refiners shutter capacity that does not come back online when peace does.

The argument that the longer the Hormuz blockade remains in this state, the more demand destruction may accumulate over the long term is the clock that oil bulls are running against. As the above-mentioned widely popular oil markets analyst Anas Alhajji points out: the indirect effects show up in places the headlines do not cover - as countries quietly de-risk from Gulf sourcing, and capital quietly de-risks from the region as a whole.

For an oil futures curve, this matters because demand destruction works against the bullish thesis on a multi-year horizon even as the front-month supply shock supports prices higher. The expression of that, classically, is a stubborn front-end backwardation paired with a structurally weaker long end. We are not there yet, but the structural setup says it’s a scenation worth watching for.

What’s next for oil prices?

This is context, not advice and, the variables that matter, in rough order of importance are as follows:

Things that could widen the gap between price and fundamentals

- Whether Fujairah remains operational without further strikes. A second drone hit on the terminal changes everything for the UAE's post-OPEC thesis and, by extension, for the long-end of the Brent curve.

- Whether OPEC+'s June production decision, which was for an increase of 144,000 barrels per day, is the first taken without the UAE in the room. How this gets treated by the market as not only serious but also symbolic. So far price actions reads it as symbolic, but we very well know that price action may be wrong, especially over the short term.

- The war-risk insurance and P&L market. Premiums, not US Navy helicopters, are the binding constraint on commercial transit. Until those normalize, "the strait is open" is a political statement, not an operational one.

- Whether Iran's "new equation" warning translates into a second coordinated salvo. The May 4th strike on the UAE may not be the response - it may be the prelude.

Things that could narrow the gap between price and fundamentals

- Any genuine bilateral channel between Tehran and Riyadh. The Saudis are not eager to underwrite Abu Dhabi's volume ambitions, which gives them an unusual incentive structure.

- Strategic-reserve releases from non-Gulf producers, particularly the US, if Washington pivots from naval to inventory tools to influence prices.

- Signs that Iran's oil-revenue position is forcing it toward negotiation rather than escalation.

The narratives that shape oil price dynamics vs real-life demand destruction

Bottom line

WTI trades around $104. Brent at $115.75. By Friday, both prices could be five dollars higher or five dollars lower, and neither outcome would invalidate the structural case that the Gulf producer order is in the middle of a regime change.

The job right now is not to call the next print. It is to keep an honest tally of the gap between what the markets are pricing and what the world is actually doing. The market is pricing a containable event. The world is doing a UAE-led restructuring of the producer cartel during a hot war over a closed waterway, with attacks on the only working bypass.

Those have been treated as separate stories. They are increasingly the same story. Position sizing, and your own thesis, should reflect the level of confidence you have that you can tell them apart in real-time.

This material is a marketing communication provided for informational purposes only and does not constitute investment advice, recommendation, or an offer or solicitation to trade. Any market analysis, opinions, or forecasts are based on publicly available information and do not constitute independent investment research. Past performance and forecasts are not reliable indicators of future results. Scope Markets accepts no liability for any loss arising from reliance on this information.

Related Articles

Technical Scope: Markets Await Fresh Catalysts

By Mohanad Yakout

Welcome to today’s edition of The Technical Scope, your twice-weekly guide to the evolving landscape of global markets through the lens of technical a...

Read More

Market Analysis

Swing Trading

Technical Analysis

Technical Scope: Markets see trend continuations

By Mohanad Yakout

Welcome to today’s edition of The Technical Scope, your twice-weekly guide to the evolving landscape of global markets through the lens of technical a...

Read More

Market Analysis

Swing Trading

Technical Analysis

Technical Scope: Price Action Ahead of the Peace Summit

By Mohanad Yakout

Welcome to today’s edition of The Technical Scope, your twice-weekly guide to the evolving landscape of global markets through the lens of technical a...

Read More

Market Analysis

Price Action

Swing Trading

Technical Analysis

Technical Scope: The Sideways trading continues

By Mohanad Yakout

Welcome to today’s edition of The Technical Scope, your twice-weekly guide to the evolving landscape of global markets through the lens of technical a...

Read More

Market Analysis

Swing Trading

Technical Scope: No changes in technicals, or fundamentals!

By Mohanad Yakout

Welcome to today’s edition of The Technical Scope, your twice-weekly guide to the evolving landscape of global markets through the lens of technical a...

Read More

Market Analysis

Technical Analysis

Swing Trading

Technical Scope: The Strong Dollar Effect

By Mohanad Yakout

Welcome to today’s edition of The Technical Scope, your twice-weekly guide to the evolving landscape of global markets through the lens of technical a...

Read More

Market Analysis

Technical Analysis

Technical Scope: Markets stuck in a sideways range

By Mohanad Yakout

Welcome to today’s edition of The Technical Scope, your twice-weekly guide to the evolving landscape of global markets through the lens of technical a...

Read More

Market Analysis

XAUUSD

USDJPY

US 500

Trend Following

Technical Analysis

Swing Trading

Support And Resistance

Stop Trading the News, Start Trading the Oil Cargo

By Victor Golovtchenko

When you see a Reuters headline that tells you OPEC+ is "completing the series of symbolic quota hikes," what exactly are you trading? When the Irania...

Read More

Market Analysis

Oil

US Oil

UK oil

WTI

Brent Crude

Trading

Technical Scope: Markets Mixed Ahead of Key Developments

By Mohanad Yakout

Welcome to today’s edition of The Technical Scope, your twice-weekly guide to the evolving landscape of global markets through the lens of technical a...

Read More

Market Analysis

XAUUSD

USDJPY

US 500

Trend Following

Technical Analysis

Swing Trading

Support And Resistance

Technical Scope: Key Levels & Market Outlook ahead of NFP Data

By Mohanad Yakout

Welcome to today’s edition of The Technical Scope, your twice-weekly guide to the evolving landscape of global markets through the lens of technical a...

Read More

Market Analysis

Chart Patterns

Candlestick Patterns

Day Trading

GBPUSD

Gold

NFP

Non Farm Payrolls

EURUSD

Oil

S&P 500

US 500

USDJPY

XAUUSD